What is Open Banking?

Introduction to Open Banking

Open banking enables financial institutions and authorized third-party providers to securely exchange financial data through APIs.

This data may encompass transaction histories, account balances, income details, and other relevant financial information.

Open banking can also be used to facilitate instant bank payments between merchants and customers. We'll explore this in more detail later, covering both AISPs (Account Information Services Providers) and PISPs (Payment Initiation Services Providers).

Open banking is poised to transform several industries by fundamentally transforming the way that merchants and customers access financial information and pay for goods and services.

The History of Open Banking

Open banking in Europe began with the introduction of PSD2 in 2018, which required banks to share payment and account data with third-party providers via secure APIs. Before this, payment solutions like GiroPay and SOFORT had already begun offering alternative ways to make online payments by facilitating bank transfers in real-time, laying the groundwork for the shift towards open banking. However, these systems were proprietary and limited in scope, whereas PSD2 opened the door to a broader ecosystem of third-party fintech providers.

Building on this, the evolving regulatory landscape has pushed further innovation with PSD3, which is expected to address emerging challenges such as enhanced security, new customer protections, and better consumer choice. New fintech providers like Ivy — the next generation of open banking in Europe — are challenging traditional banks and established players like GiroPay and SOFORT by delivering a more flexible, user-friendly approach to open banking payments for both merchants and customers.

How is Open Banking Used?

Instant Payments

Open banking enables instant, account-to-account transfers, reducing the need for costly intermediaries like credit card networks and digital wallets. This streamlined approach helps businesses lower transaction fees and enhance payment efficiency.

Recurring Payments

Open banking enables automated setup of SEPA Direct Debit mandates, streamlining payment processing by eliminating manual IBAN entry, reducing fraud risk, and minimizing chargebacks. This automation accelerates payment initiation and enhances security, making recurring payments more efficient for businesses and consumers alike.

Instant Payouts

Open banking enables faster and more secure payouts by facilitating direct account-to-account transfers. This approach reduces reliance on traditional intermediaries, streamlines processing times, and minimizes transaction costs, offering businesses an efficient solution for disbursing funds to customers or partners.

Payment Reconciliation

Open banking can simplify the payment reconciliation process for business by giving third-party applications access to customers’ financial information, allowing them to easily match incoming payments with invoices. This reduces administrative burden and reduces the risk of manual errors.

Identity Authentication

Businesses can use open banking to authenticate customer identities by verifying their bank credentials. This helps mitigate the risk of identity theft and fraud, especially in online transactions.

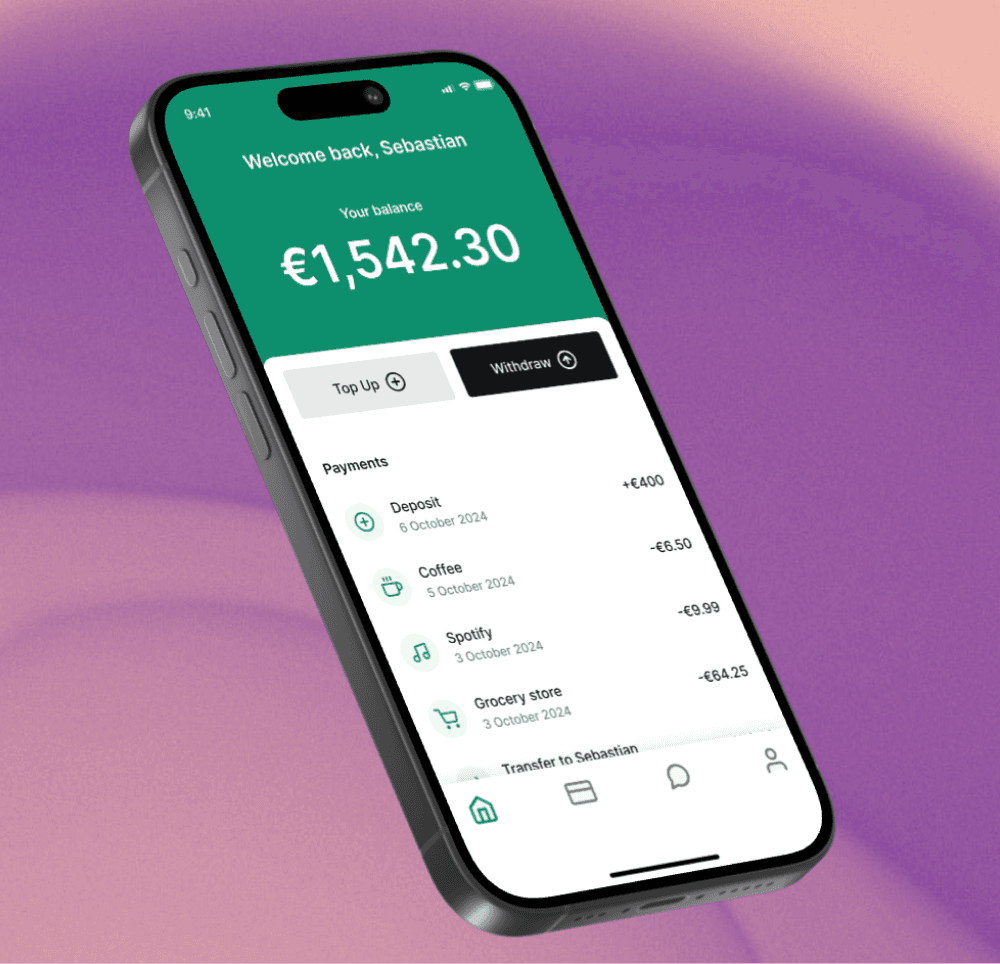

Financial Management

Open banking enables third-party providers to develop applications that support a range of financial management activities, including budgeting, saving, and expense tracking. These services enhance financial transparency and empower individuals to make more informed financial decisions.

Open Banking Benefits

For Businesses

Open banking offers significant benefits for businesses that deal in both physical goods (i.e., eCommerce and retail) as well as digital goods and services like crypto, gaming, and financial services.

Lower

Payment Costs

By cutting out expensive intermediaries like credit card networks and digital wallets, open banking enables businesses to save up to 90% on every transaction.

Expanded

Payment Options

Open banking gives businesses a way to offer a safe, reliable, and convenient payment method for customers who may not have access to credit cards and digital wallets.

Resilient

Payments Infrastructure

Open banking provides businesses with a resilient payments infrastructure by enabling direct, bank-to-bank transactions that reduce dependency on traditional payment networks and enhance system reliability.

Operational

Agility

Open banking enhances cash flow by enabling faster, direct payments that reduce processing delays and improve fund availability for businesses.

For Consumers

It isn’t just businesses that stand to benefit from open banking. Consumers have a lot to gain too.

Simplified

Finances

With open banking, consumers can simplify their finances by decreasing their dependence on several different accounts, payment methods and third-party apps. All financial transactions are securely carried out through their primary bank accounts and banking app.

Greater

Convenience

Open banking removes many of the inefficiencies associated with traditional payment methods, such as manual data entry at checkout or disruptions due to credit card limits. By simplifying these processes, open banking enhances convenience and delivers a smoother customer experience.

Less

Risk

Open banking offers a significantly safer alternative to traditional card and wallet payments, as consumers are not required to input card details or rely on third parties to securely store sensitive information. Additionally, Open banking legislation empowers consumers with full control over their financial data, allowing them to decide precisely who has access and for what purpose, enhancing both security and transparency.

How does Open

Banking Work?

Open banking leverages APIs to securely transfer data between financial institutions (like banks and credit unions) and authorized third-party providers. Data is encrypted every step of the way. The three kinds of APIs that are most commonly used in open banking include:

Data APIs: These provide read-only access to data like transaction history and account balances.

Transaction APIs: These enable the initiation of payments, such as funds transfers or direct debit setups.

Product APIs: These are used by third-parties (like comparison websites and marketplaces) to collect and display information about products, rates, and terms.

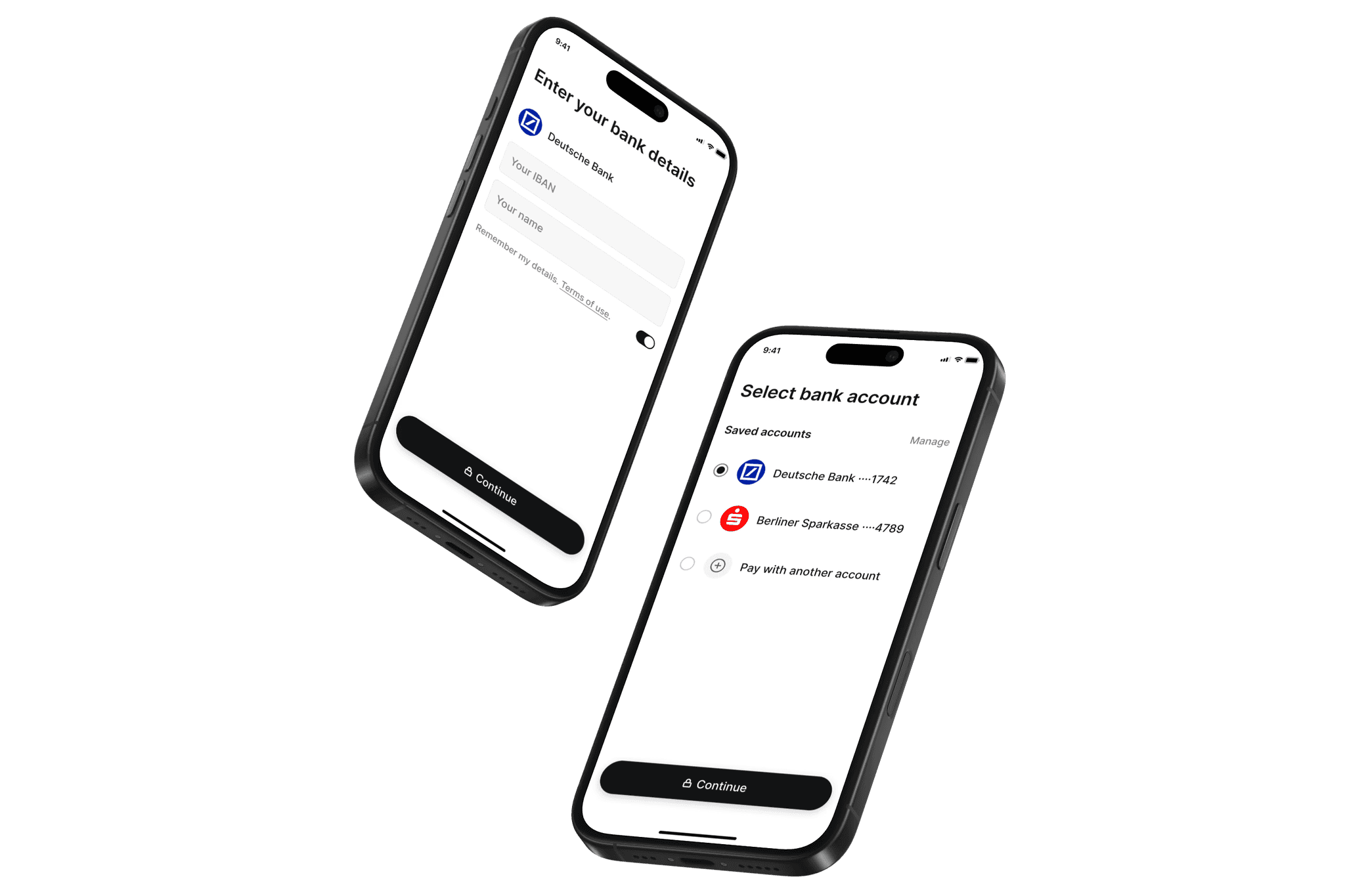

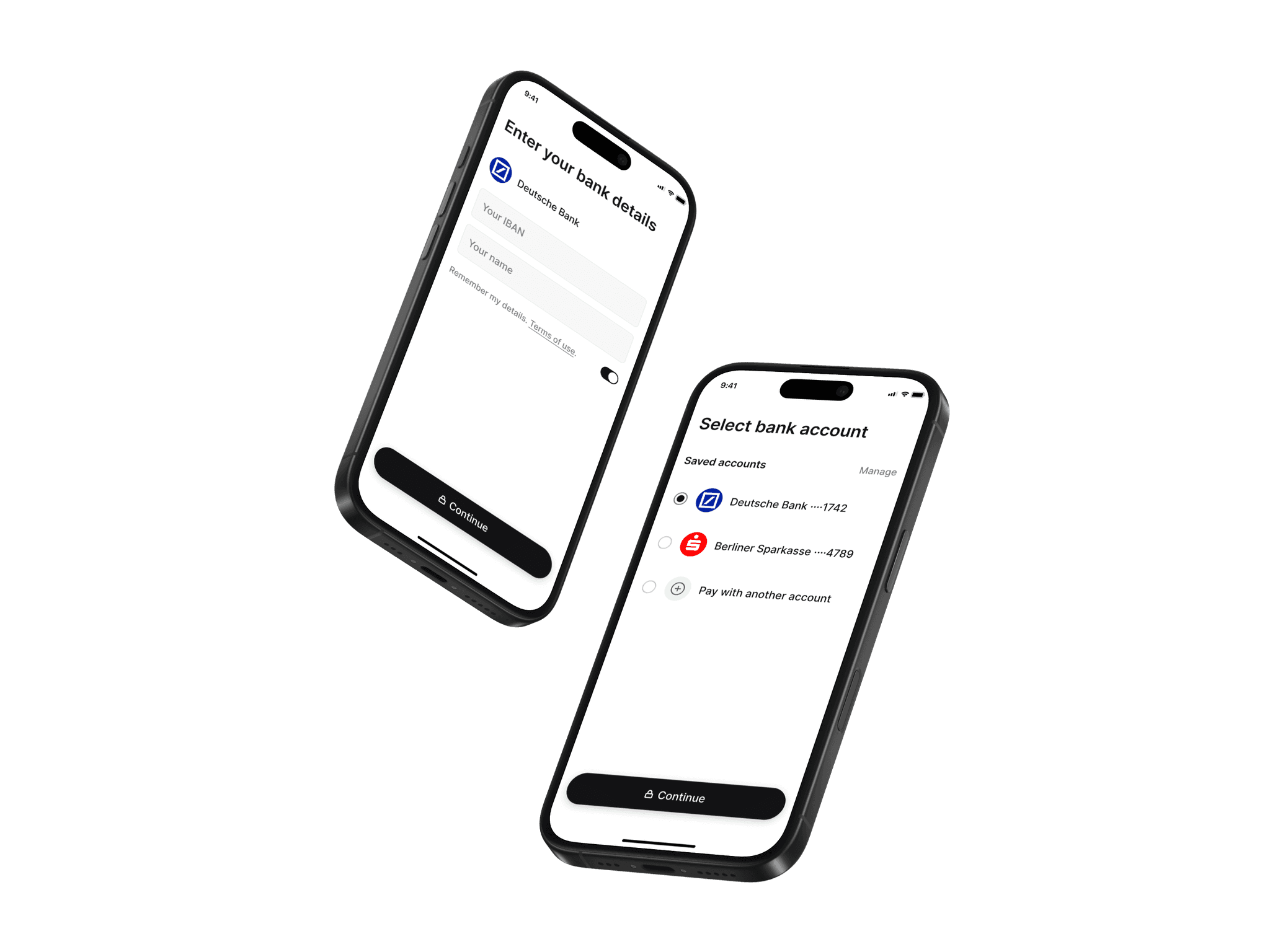

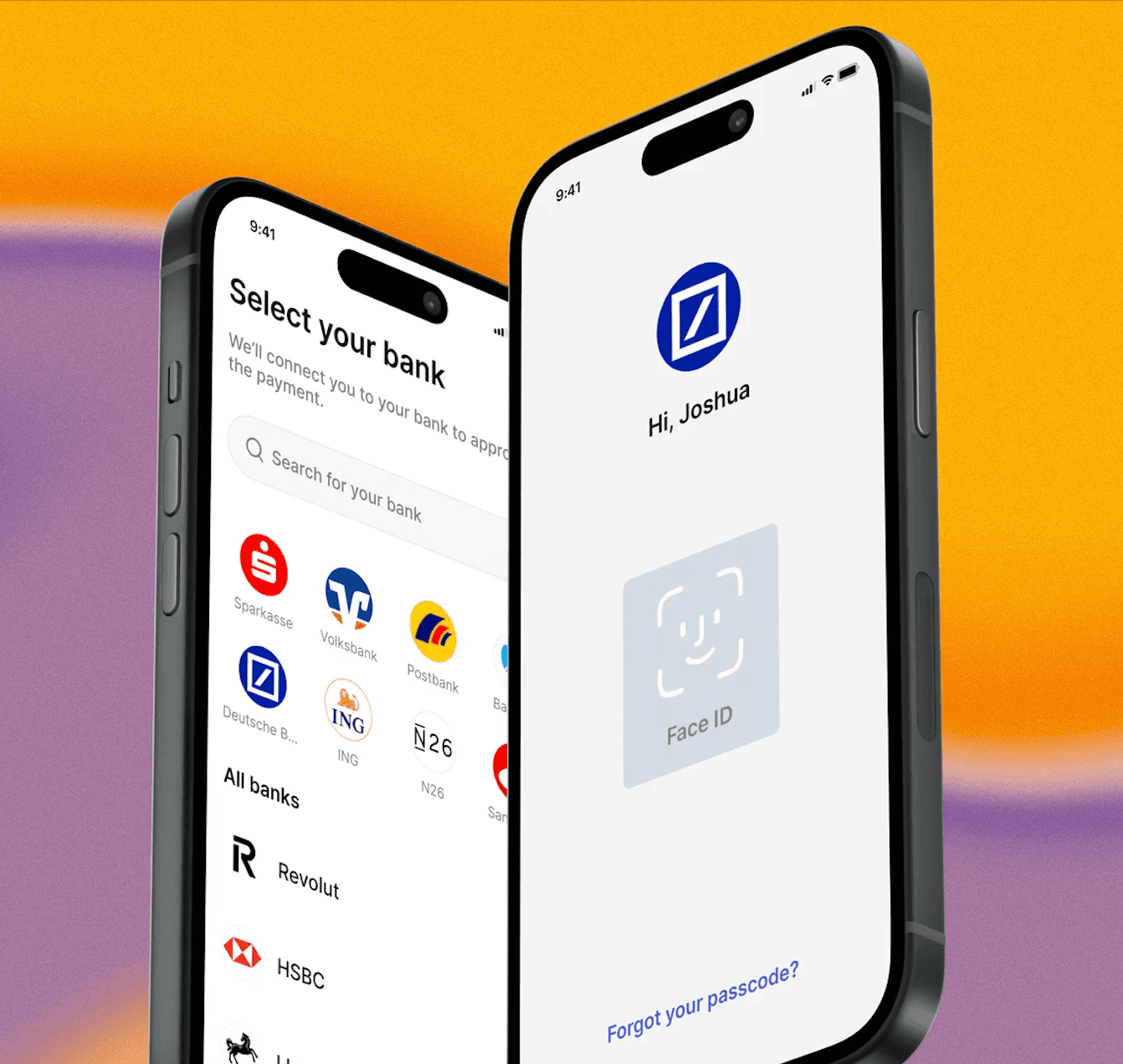

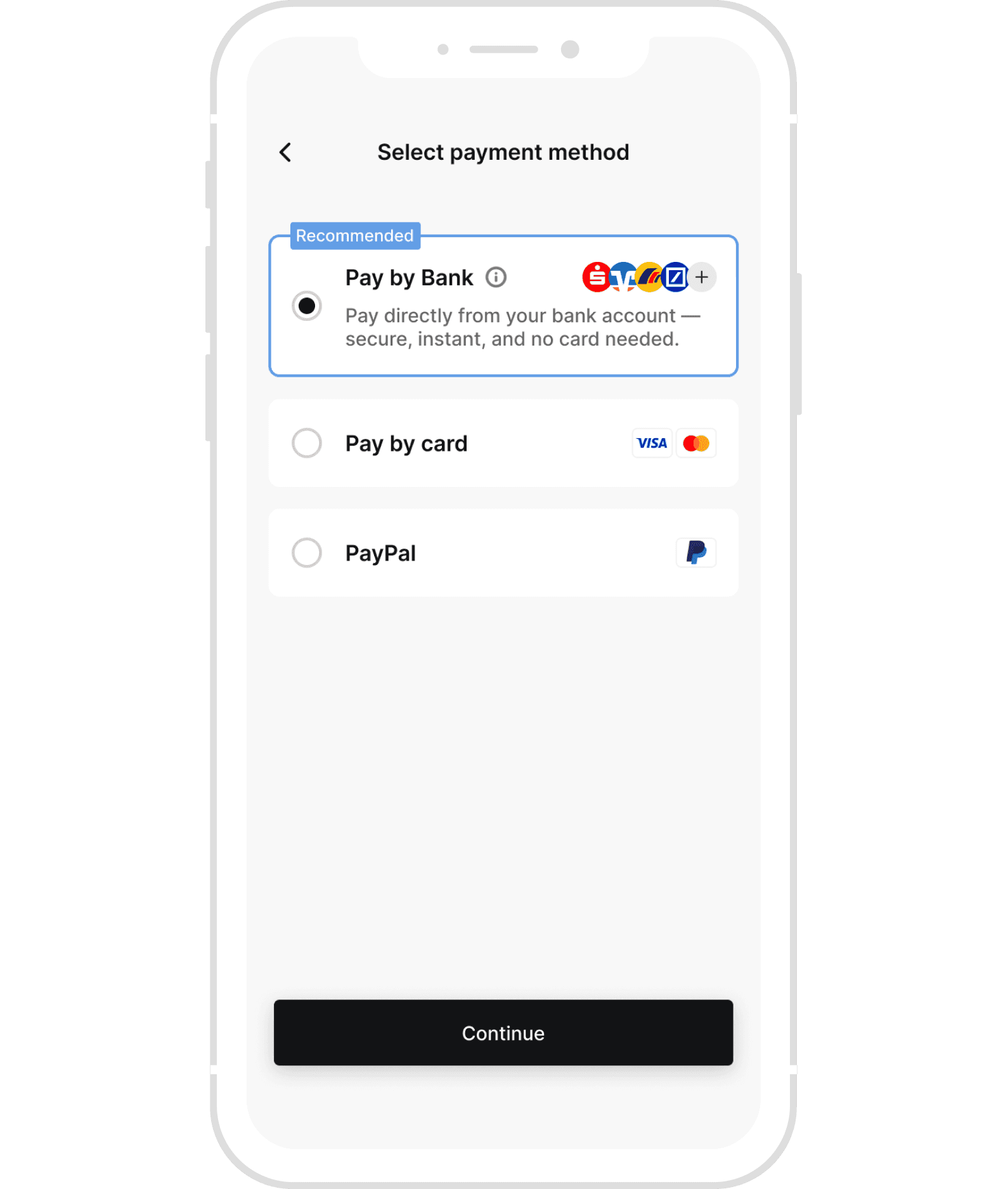

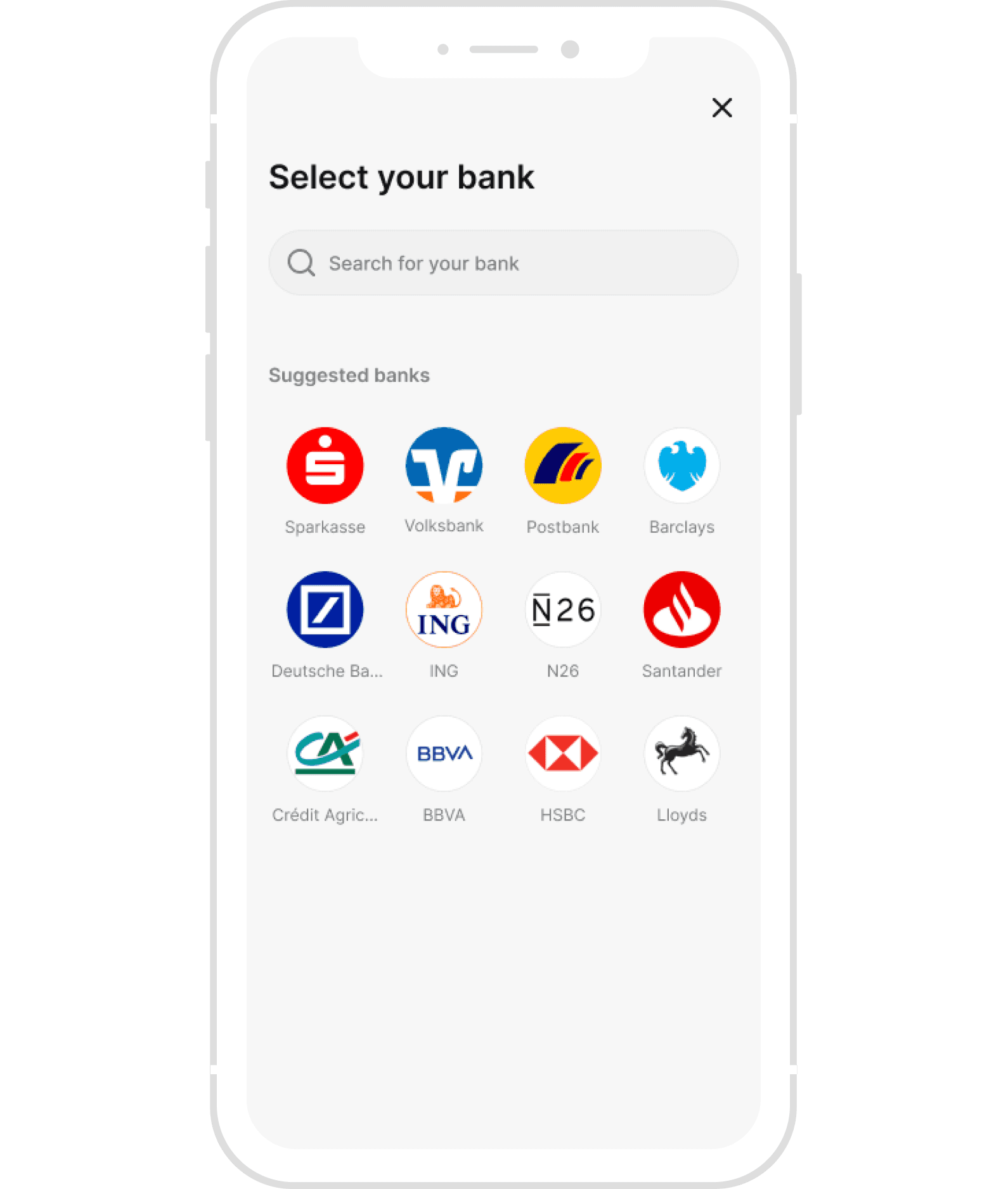

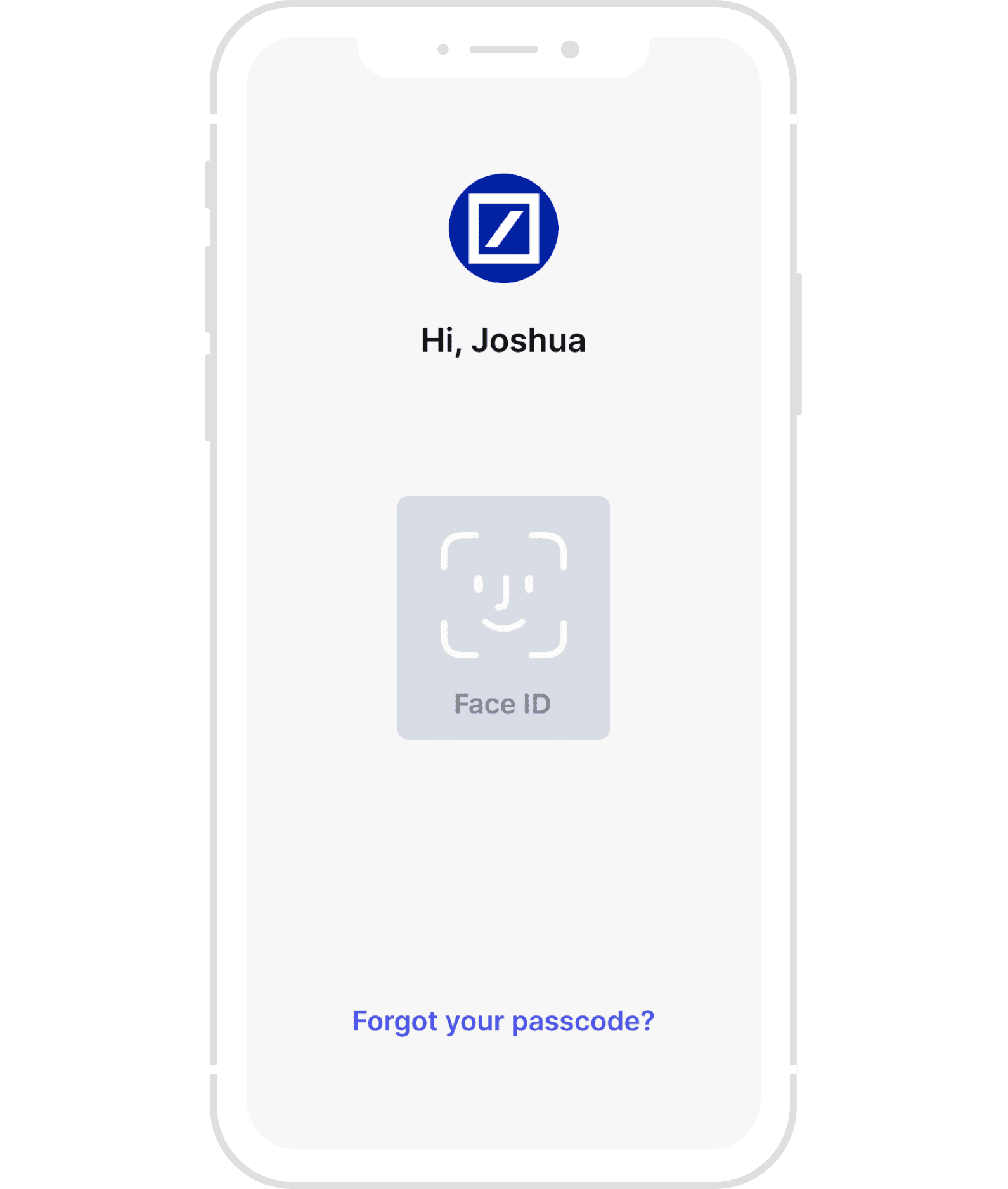

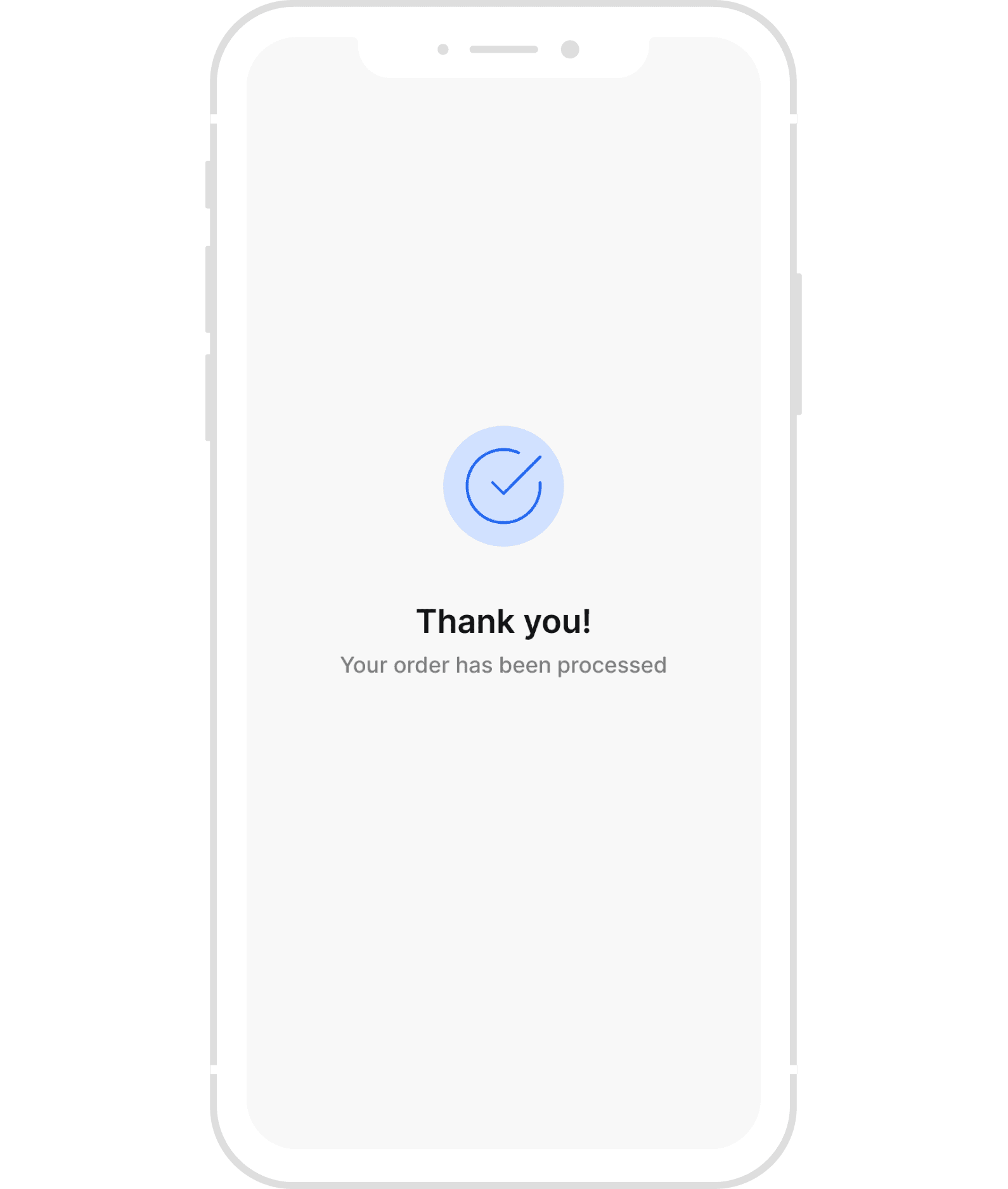

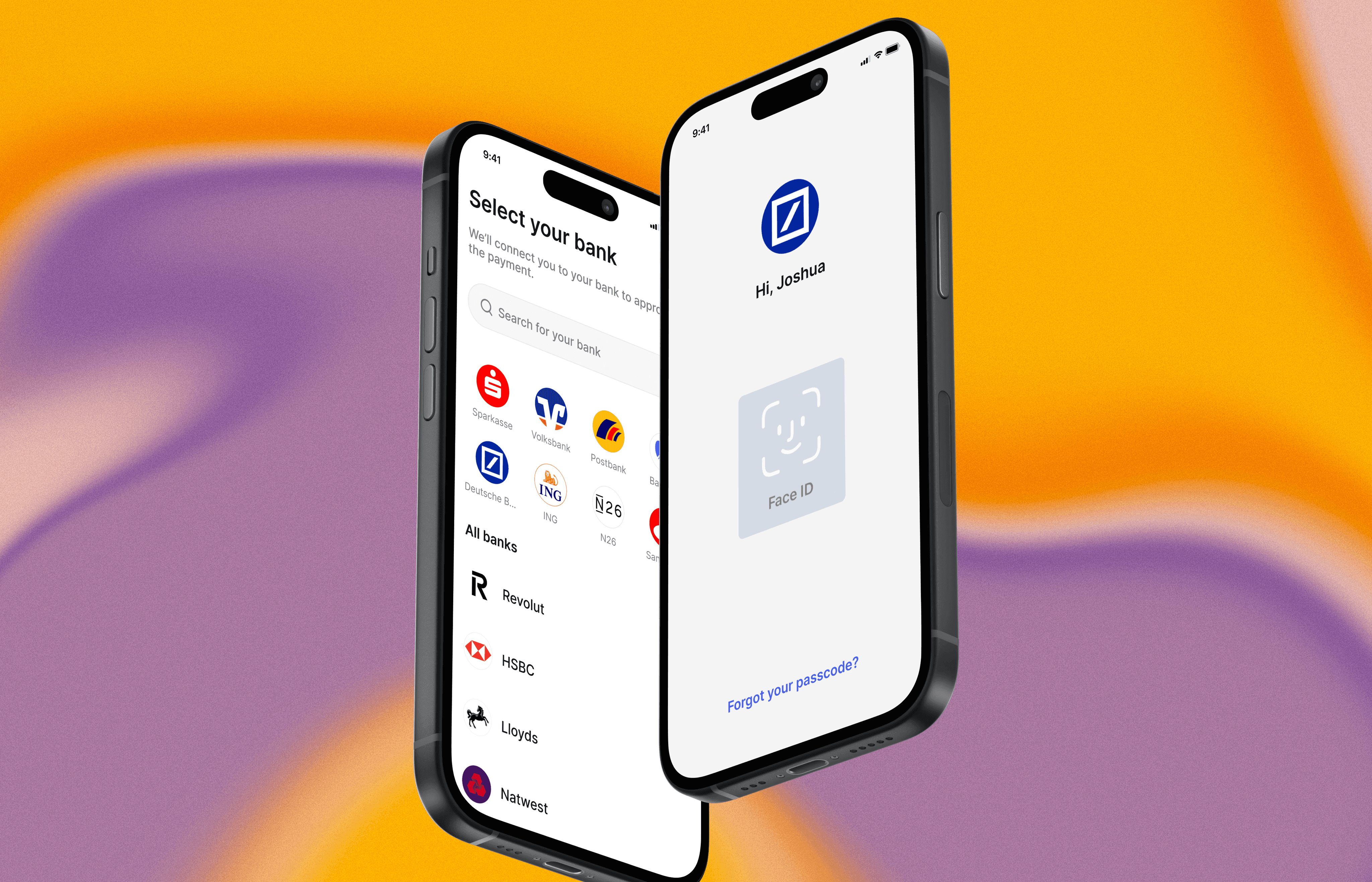

Click through the explainer below to see open banking in action. This use case illustrates how a consumer can make a payment to an online merchant directly from their bank account. There’s no need to manually enter credit card details or create new accounts — customers simply select their bank and securely authorize the payment within their banking app.

What are Third Party Providers (TPPs)

in Open Banking?

Third Party Providers (TPPs) are authorized organizations that use APIs to access customers’ financial information in order to provide a range of services. They typically fall under two categories:

01

Payment Initiation Service Providers (PISPs)

These are authorized third parties that facilitate payments directly from a customer’s bank account to a merchant, without requiring a card or separate account setup.

02

Account Information Service Providers (AISPs)

These are authorized third-party services that aggregate and provide customers with access to their financial data from multiple accounts, enabling better financial management and insights.

Is Open Banking Safe?

Yes, open banking is completely safe. Consumers maintain full control over their financial data and must provide explicit consent to access and share it. Additionally, they do not have to share security credentials or rely on anyone to store sensitive information like credit card details. All authentication is securely handled through their banking app, using passwords, PINs, or biometric methods.

Third-Party Open Banking Providers (TPPs) undergo rigorous certification processes to obtain authorization and are required to uphold the highest standards of security and privacy, including compliance with data protection regulations such as GDPR.

Open Banking in Numbers

70

regions

across the world are rolling out open banking infrastructure

69%

year-on-year growth for open banking payments

63.8

million

Open banking users in Europe by 2024

What are the Factors that are

Driving Open Banking Adoption?

For Consumers

The reasons consumers opt for open banking payments is convenience, speed and security.

Convenience: Unlike credit cards and digital wallets, there is no need to manually enter payment details at checkout or create an account. All consumers have to do is choose their bank at checkout to initiate the transaction.

Speed: Once the consumer has selected their bank, they’re redirected to their primary banking app from where they can authorize the payment in seconds. The transaction is immediate: funds are transferred instantly from the consumer's bank account to the merchant’s.

Security: Because all transactions are securely authorized from a consumer's bank app using passwords, pins, or biometric identification, they don't have to worry about third-party websites storing their credit card or account information.

For Businesses

For businesses, open banking offers a few major advantages, including:

Cost-effective: Credit cards and digital wallets have high add-on fees for every transaction. Open banking is significantly cheaper, offering merchants up to 90% cost savings when compared to cards and wallets.

Reduces chargeback risk: There is no chargeback mechanism with open banking payments. Funds are transferred instantly from the customer’s bank account to the merchant’s.

Improved cash flow: Because funds are transferred instantly, merchants have improved access to cash flow.

Regulatory compliance in Open Banking

Open banking is subject to stringent regulatory requirements.

These differ between countries. Some of them include:

PSD2, PSD3 & PSR – Europe

The EU’s PSD2 directive mandates secure, standardized access to consumer banking data for authorized third-party providers. PSD2 also enforces Strong Customer Authentication (SCA) to reduce fraud. PSD3 and PSR are a new set of legislative proposals that are the evolution of PSD2. Their purpose is to further harmonise the European payments landscape and reduce regional variance.

CDR (Consumer Data Right) – Australia

Australia's Consumer Data Right gives consumers control over their data across various sectors, starting with banking (Open Banking). The Australian Competition and Consumer Commission (ACCC) oversees CDR, which mandates that authorized data recipients use secure APIs for access and data sharing.

Open Banking Standards – United Kingdom

Initiated by the UK’s Competition and Markets Authority (CMA), Open Banking standards require the nine largest UK banks to provide secure APIs for customer data access and payment initiation. These standards are supported by the Open Banking Implementation Entity (OBIE) and align closely with PSD2.

Ley Fintech (Fintech Law) – Mexico

Mexico’s Fintech Law regulates open banking by requiring banks to establish APIs for secure data sharing with third-party providers, promoting financial inclusion and competition. The law is enforced by the Comisión Nacional Bancaria y de Valores (CNBV).

CFPB Section 1033 – United States

The Consumer Financial Protection Bureau (CFPB) has proposed regulations under Section 1033 of the Dodd-Frank Act, which will provide consumers with rights to access their financial data and authorize secure data sharing. While formal rules are still evolving, several U.S. banks have voluntarily adopted secure APIs.

Open Finance Framework – Brazil

Brazil’s Open Finance framework, developed by the Central Bank of Brazil, expands beyond traditional open banking to include insurance, pensions, and investments. The regulation establishes mandatory API-based data sharing for financial institutions, aiming to increase competition and financial accessibility.

Open Banking with Ivy – Powering Europe’s Biggest Businesses

Ivy represents the next generation of open banking providers and is the trusted open banking partner for leading European companies. Here’s why:

Leading

Conversion

Ivy offers optimised conversion rates through smart routing, selecting the highest converting payment rail from our large payment provider network.

Best-in-Class Connectivity

Ivy allows you to tap into over 5,000 banks across Europe through a single API, powered by our extensive network of local connectivity providers.

Optimized

Adoption

Ivy is a fully customizable white-label solution, seamlessly integrating with your brand, fostering trust, and boosting customer adoption.

For companies seeking optimal conversion rates, Ivy’s Smart Routing Engine offers a powerful advantage. By dynamically optimizing payment flows, Ivy intelligently selects the highest-converting provider from its extensive network of connectivity partners for each transaction. This advanced routing minimizes payment failures, ensuring a smooth and uninterrupted payment experience. As a result, companies benefit from higher transaction success rates and improved customer satisfaction, making Ivy a valuable partner for businesses that prioritize seamless payment processing and a high-quality customer experience.

In addition, Ivy provides unmatched connectivity across Europe, linking to over 5,000 banks across the region. With Ivy's best-in-class European coverage, businesses can offer seamless, instant payments to customers anywhere in Europe. As traditional payment options like GiroPay and SOFORT phase out, Ivy’s extensive network ensures a smooth transition to a future-proof, reliable payment experience —delivering consistent performance and an exceptional customer experience across all European markets.

Finally, Ivy offers a fully white-label solution, allowing seamless integration into your existing brand to maintain consistency and build customer trust. By aligning with your established brand identity, Ivy minimizes barriers to user adoption, creating a frictionless experience that encourages customers to choose this option at checkout as opposed to cards and wallets.